Good Afternoon!

Good Afternoon!

The Spring Market has officially arrived and demand is poised to

continue its spring surge.

Spring Market: Over the next month, demand will rise to its highest levels of the year, where it will remain through the end of Spring.

The Orange County housing market did not look at all like 2015 after the first couple of months of the year. Instead, it looked a lot like it was going to be 2014, a year with a bit less demand and an inventory that continuously grew on the backs of overpriced homes. After ringing in the New Year, stocks were diving, prices at the gas pump were dropping to levels not seen in many years, and there was quite a bit of uncertainty in the air. All of these factors were a drag on the county’s housing market and there was a delay in the start to the Spring Market. Typically, the local market revs its monstrous engine right after the Super Bowl. Instead, demand was off by 11% throughout February. Where was housing heading? Would there be a correction in pricing? Is it still a good time to buy? Are we moving towards an economic slowdown?

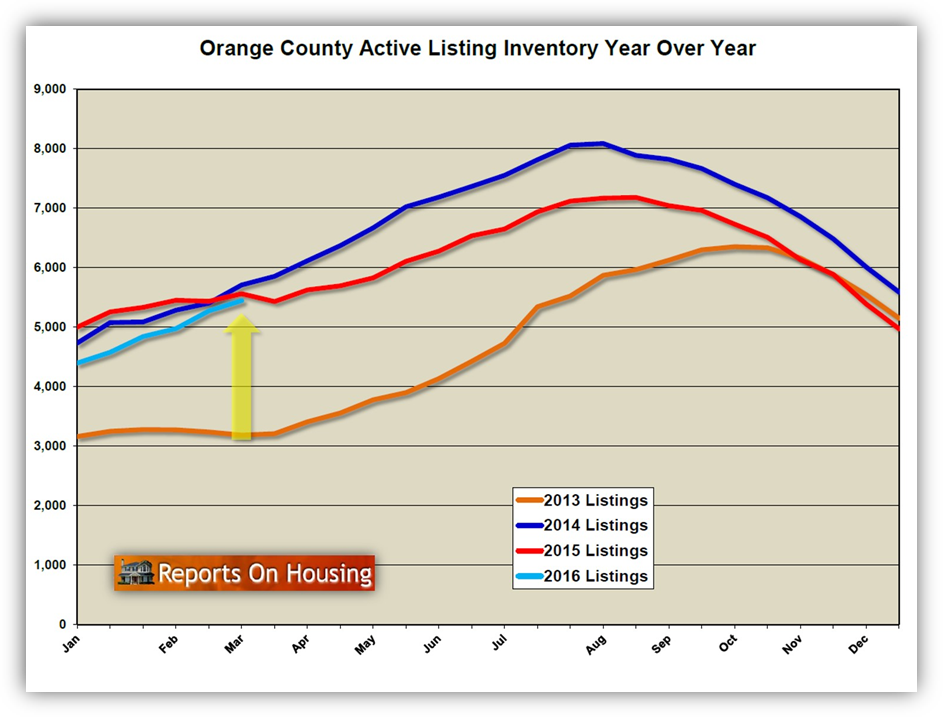

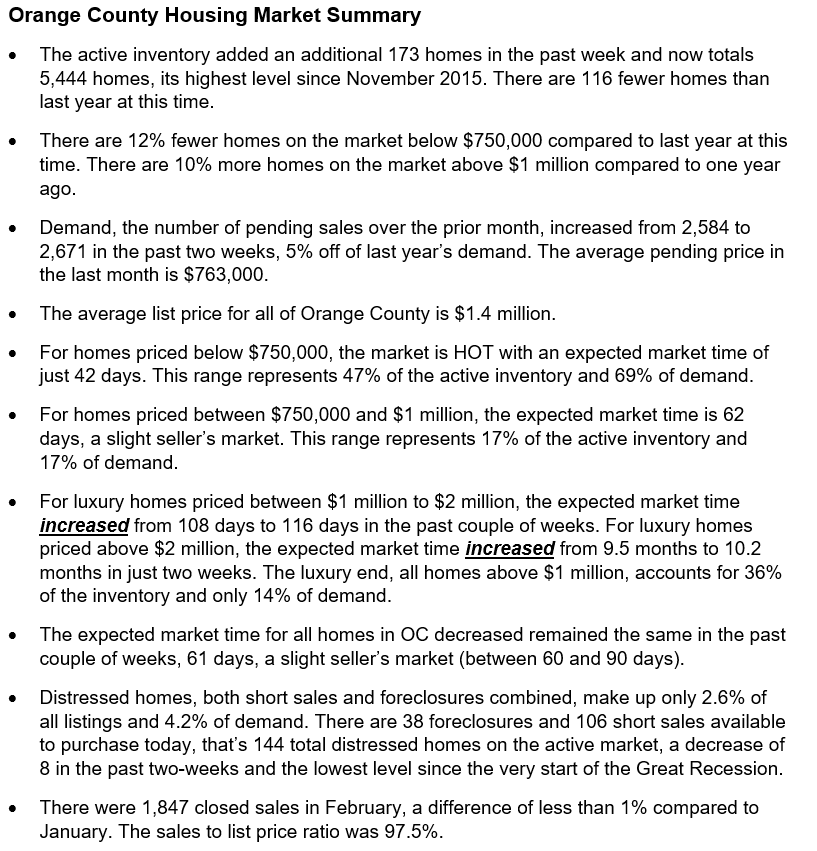

The trend for this year is that housing is NOT headed for a correction; not anytime soon. Nationally, and especially locally, there has been a real supply issue that dates back to 2012. For this time of year, the average active inventory for Orange County since 2005 is 8,766 homes. Currently, we are at 5,444 homes. That means it is off by 38%. Since 2012, the average inventory for this time of year has been 5,349 homes. REALTORS® are not exaggerating when they state that there are not enough homes on the market. It is an absolute fact. With extremely favorable interest rates, there is tremendous demand. Strong demand coupled with a low supply means that the real estate market favors sellers, not buyers. The expected market time, the time it would take, on average, to list a home and place it under contract, is 61 days. The year started with an expected market time of 81 days and has been dropping ever since. In order for the market to shift in favor of buyers, the inventory would have to rise and demand would have to drop. The expected market time would have to exceed 120 days, double from where we are today. That is just not going to happen, not anytime soon.

Now that the stock market has turned around, along with a rise in oil prices, it looks as if it is now business as usual for our economy and the local housing market. The anxious start to housing has shifted back to the fact that it is a good time to buy and buyers want to take advantage of the very low interest rate environment. Everybody gets it, as soon as the economy starts rolling along again, the Federal Reserve is ready to raise the short term interest rate again. Long term rates may not rise by much over the course of this year, but everybody knows that the low rates today cannot stick around forever. Naturally, buyers want to buy now while they know for certain that they will be able to cash in on a great rate. If interest rates were to jump from 4% to 5% (and, someday they will), the payment for January’s median priced home, $618,500, at 20% down would climb from $2,362 to $2,656, an increase of $294 per month, or $3,528 per year.

Now that the stock market has turned around, along with a rise in oil prices, it looks as if it is now business as usual for our economy and the local housing market. The anxious start to housing has shifted back to the fact that it is a good time to buy and buyers want to take advantage of the very low interest rate environment. Everybody gets it, as soon as the economy starts rolling along again, the Federal Reserve is ready to raise the short term interest rate again. Long term rates may not rise by much over the course of this year, but everybody knows that the low rates today cannot stick around forever. Naturally, buyers want to buy now while they know for certain that they will be able to cash in on a great rate. If interest rates were to jump from 4% to 5% (and, someday they will), the payment for January’s median priced home, $618,500, at 20% down would climb from $2,362 to $2,656, an increase of $294 per month, or $3,528 per year.

So, we are not headed for an economic disaster, no slowdown, no correction in housing, and interest rates remain low. As a result, housing is springing forward and demand is back. However, prices are not surging. Home prices are much higher than they were back in the beginning to 2012, the real start to the housing turnaround. Buyers do not have the stomach to pay much more than the last comparable sale. They want to pay the Fair Market Value for a home, which can be determined by carefully considering the most recent pending and closed sales. Prices may rise a bit during the first half of 2016 in the lower price ranges, below $750,000, but they are not going to surge.

Active Inventory: The inventory increased by 3% in the past two weeks.

The active inventory increased by 173 homes, or 3%, in the past two weeks and now sits at 5,444. After a very slow start to the year, when far fewer homes were coming on the market compared to 2015, the trend has reversed course. To date, there are only 45 fewer homes that have come on the market compared to last year. As a matter of fact, over the last month, 3% more homes came on the market. On January 1st, there were only 4,396 homes on the market. Since then, the inventory has added an additional 1,048 homes.

In order for the active inventory to grow, more homes have to come on the market than go off the market. The only way for a home to come off the market is for a home to move to pending status or for a seller to pull their home off the market and throw in the towel. With the beginning of the Spring Market, we know that sellers are not throwing in the towel. So, the increase in the inventory is indicative of an accumulation of homes that stay on the market without being able to procure an acceptable offer to purchase. The biggest culprit during the spring to successfully selling are the sheer number of overpriced homes. Most homeowners start off a bit overzealous and unrealistically price their homes. In time, the market illustrates that a reduction in price is necessary in order to find success.

Last year at this time the inventory totaled 5,560 homes, 116 more than today, with an expected market time of 1.98 months, or 59 days, a slight seller’s market. Today’s expected market time is at 2.04 months, or 61 days, still a slight seller’s market. A slight seller’s market means that there is not much price appreciation but sellers get to call more of the shots in terms of negotiating the finer details of a contract.

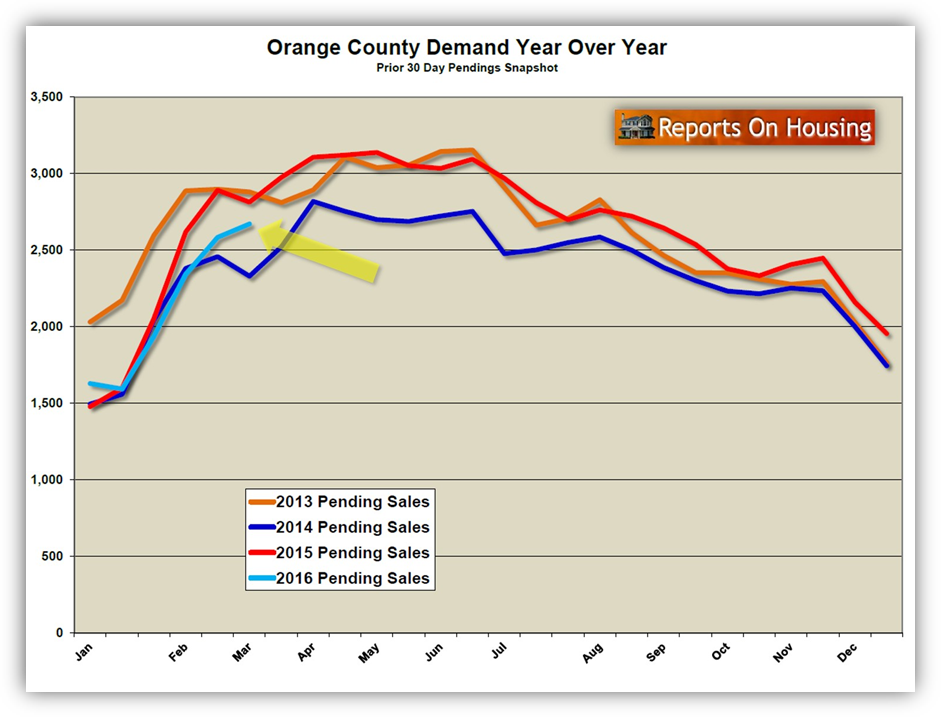

Demand: In the past two-weeks demand increased by 3%

Demand, the number of new pending sales over the prior month, increased by 87 homes in the past two-weeks, and now totals 2,671, the highest level since August of last year. Today’s demand is not as good as 2015, currently 5% less, but much better than 2014, 15% higher. The disparity from last year is growing smaller and is poised to continue to surge over the course of the next month. Last year at this time demand was at 2,813, that’s 142 additional pending sales. Two weeks ago the disparity was 307.

Summary:

[gravityform id=”22″ title=”true” description=”true”]

Leave a Reply